This article is an onsite version of our Europe Express newsletter. Sign up here to get the newsletter sent straight to your inbox every weekday and Saturday morning

Welcome back. Thinking about Europe’s future means joining up the dots. What does this entail in practice? I’m at tony.barber@ft.com.

Among the preoccupations of most EU governments are the maintenance of military and financial support for Ukraine; boosting Europe’s defence capabilities; addressing climate change; and grappling with the political insurgencies of upstart rightwing nationalist parties.

What links these different challenges is that success in dealing with them depends to a large degree on a strong European economy.

So this week I hope to join up the dots by outlining how the outlook for economic growth, competitiveness and the public finances will affect Europe’s ability to support Ukraine, raise defence spending, combat climate change and strengthen political stability across the continent.

In the last resort, Europe’s economic performance matters because it is inextricably connected with the protection of liberal democracy and with the preservation — or, better, the modernisation — of its distinctive post-1945 social contract, based on a combination of capitalism and the welfare state.

Schnabel and the social fabric

One policymaker who joins up the dots with admirable insight is Isabel Schnabel, the German member of the European Central Bank’s executive board. In February, she gave a speech in Florence that explained where Europe’s economic performance is falling short.

Among the points she mentioned:

-

Too few companies are reaping efficiency gains from information and communication technologies

-

Product and labour markets are over-regulated

-

The venture capital industry is too small

-

Societies are rapidly ageing, and more people prefer to work fewer hours

-

The momentum of economic reform has slowed since 2012

The most important sentence of Schnabel’s speech reads as follows:

To assert its role, the euro area needs to remain competitive; it must be capable of creating the sustainable growth that our social and economic fabric depends on [my italics].

The southern mirage

On the question of growth, the FT’s Martin Arnold wrote an eye-catching article this week that described how southern Europe’s largest economies — Greece, Italy, Portugal and Spain — have outperformed Germany since 2017.

Does this mean that economic convergence between northern and southern Europe, an ambition of EU policymakers since the euro’s birth in 1999, is finally happening? Or is the picture of southern success misleading?

One clue is contained in Martin’s article, which quotes Yannis Stournaras, Greece’s central bank governor, as saying that the southern economies’ recent outperformance was in many ways just a reflection of German underperformance. “I don’t think this is permanent,” Stournaras said.

That’s a good point — and one underlined in a commentary by Lorenzo Codogno, a former director-general of the Italian Treasury, for the newspaper Il Riformista. He writes (here in Italian):

Italy has been in structural decline, and not just since the 1990s … Total factor productivity … has stopped growing since the mid-1970s.

Since the 1970s, Italy has artificially propped up its GDP growth with continuous devaluations of the lira and an enormous expansion of public debt. But once these artifices were no longer possible with the process of convergence towards monetary union, GDP stopped growing.

What about the reforms supposedly launched in Italy to draw on tens of billions of euros in grants and loans from the EU’s post-pandemic recovery fund? Codogno is sceptical:

The impression is that the current efforts are aimed at ticking the boxes agreed with the EU to obtain new funds without the current government convincingly taking ownership of the reform process.

Public finances under strain

The problem is as follows: less economic reform means lower long-term sustainable growth, and lower growth means less to spend on Ukraine, defence and climate change. It may also mean less to spend on schools, transport, healthcare and domestic social programmes of the kind needed to persuade at least some citizens not to transfer their votes to rightwing nationalist parties.

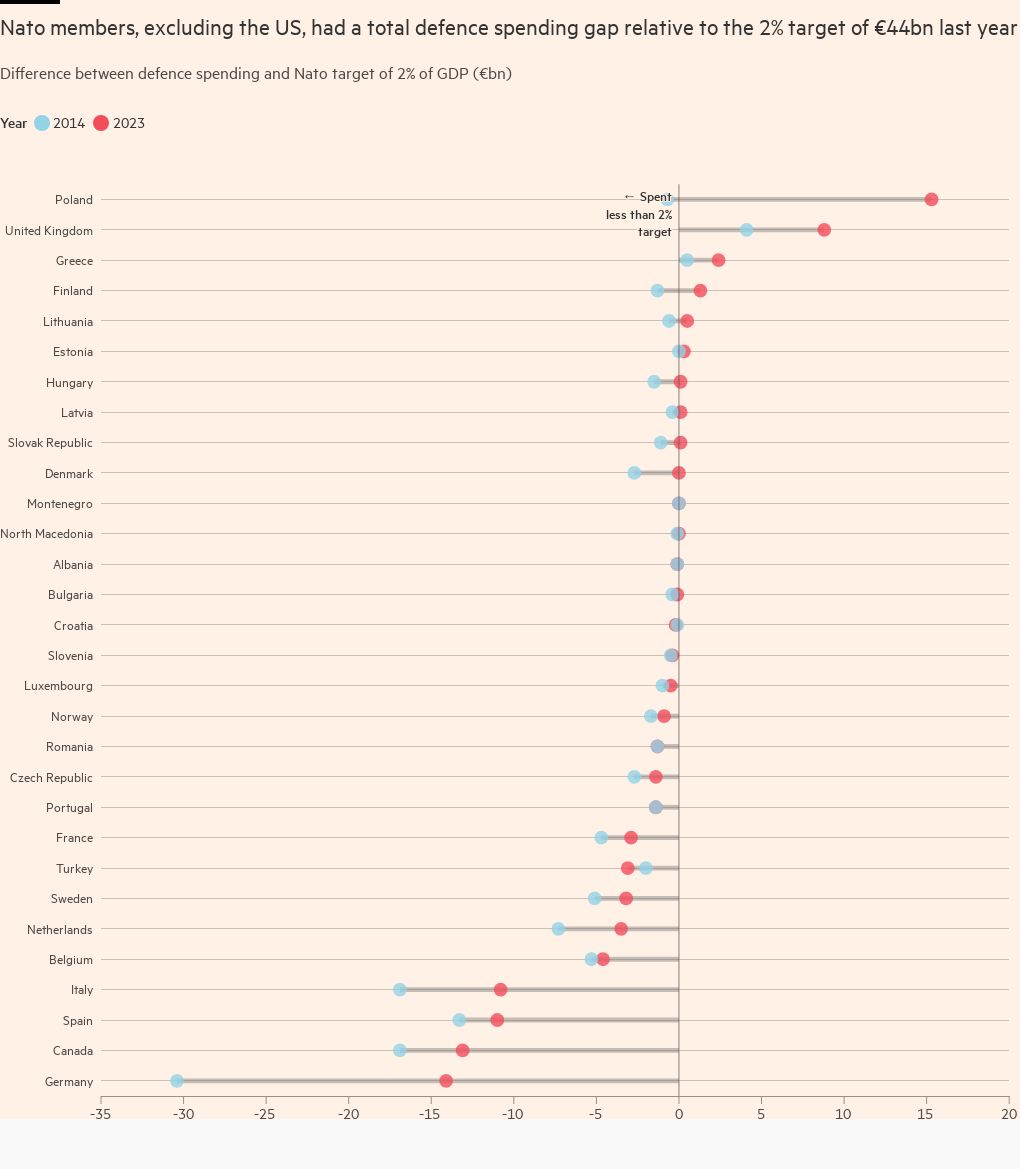

These pressures are visible in the struggle of some European governments to keep budget deficits and public debt under control. According to research from Germany’s Ifo Institute, quoted in this FT story, many countries that fall short of meeting Nato’s target of spending at least 2 per cent of GDP on defence are precisely those with high deficits and debt.

Climate change costs

Then there are the costs of action on climate change. According to Mario Draghi, the former Italian premier and ECB president, who is due to release a report later this year on European competitiveness, the EU’s planned green and digital transitions will require annual expenditure of €500bn.

Some governments with overburdened public finances are already anxious about how to meet the EU’s legally binding target of a “climate-neutral” economy by 2050 — that is, an economy with net-zero greenhouse gas emissions.

Bruno Le Maire, France’s finance minister, recently criticised “the Europe we no longer want, which sets targets that are too restrictive and which are not satisfactory climate targets”.

Many Europeans who will have to pick up part of the tab for climate change policies — for example, by giving up diesel cars or paying higher fuel taxes — are susceptible to the allure of hard-right parties or anti-establishment movements. This was the lesson of the gilets jaunes (“yellow vests”) protests in France in 2018-2019.

French deficit shock

One of Europe’s biggest economic stories last month was the news that France’s 2023 budget deficit rose to 5.5 per cent of GDP, up from 4.8 per cent in 2022 and far above the government’s 4.9 per cent forecast.

Up to 2027, France will have to find tens of billions of euros in savings at precisely the time when it will be under pressure to allocate funds for Ukraine, defence expenditure and climate change.

Bear in mind that France has not balanced its budget since 1974. As the Scope credit rating agency observes:

“The scale of the review is unprecedented for a country having an uneven record of significantly and sustainably reducing public expenditures.”

Macron’s government lacks a parliamentary majority, so it is unclear how it can push through budget savings without the support of opposition legislators. They have little interest in extending a lifeline to figures such as Le Maire and Gabriel Attal, the recently appointed prime minister, each of whom may plan to run in the 2027 presidential election.

In this way, we see how modest economic growth and strained public finances may have serious political repercussions. The party tipped to come first in France in the June elections to the European parliament is Marine Le Pen’s hard-right Rassemblement National. She will hope to exploit public discontent with France’s budget crunch and ride a wave of support all the way to 2027.

Germany: is decline overstated?

Germany has a public finances problem, too — in some ways, a self-inflicted one. In 2009, Angela Merkel’s government amended the constitution to enshrine a commitment to near-balanced budgets. Now that commitment stands in the way of much-needed expenditure on greening and modernising the German economy — not to mention boosting defence spending.

As in France, the roots of Germany’s problems — which include low long-term growth rates — are deeper. Wolfgang Münchau, writing in the New Statesman, says:

Germany’s current trajectory is not just the downward part of your average economic cycle. The great age of “Made in Germany” — of German manufacturing and engineering excellence — is drawing to a close.

Not everyone buys Wolfgang’s argument. In this commentary for the IMF, Kevin Fletcher, Harri Kemp and Galen Sher say:

Concerns about widespread deindustrialisation are … overstated. While the energy-intensive chemicals, metals and paper industries have contracted, they only account for 4 per cent of the economy.

Bigger issues, they say, are sluggish productivity growth, an ageing population, insufficient digitalisation and inadequate investment in public infrastructure (see chart by the IMF below).

Whatever the causes of Germany’s economic difficulties, the outcomes are similar to those in France: public hostility to costly aspects of the green transition, and a rise in support for the hard-right Alternative for Germany party, now lying second in opinion polls.

Taken as a whole, there seems be a mismatch between Europe’s ambitions with regard to Ukraine, defence, climate change and other areas that require large-scale spending on the one hand, and low economic growth and stretched public finances on the other.

It seems to me that, in order to avoid ceding political ground to hard-right nationalist parties, Europe’s governments will be under increasing pressure to scale back some of their ambitions. Will it be defence? Will it be climate change? For how long can hard choices be put off?

The first 25 years of the euro — a policy paper by Marco Buti and Giancarlo Corsetti for the Centre for Economic Policy Research

Tony’s picks of the week

For Turkey’s secular-leaning Republican People’s party, last weekend’s municipal elections marked not just a victory over President Recep Tayyip Erdoğan but its biggest electoral success in almost half a century, the FT’s Adam Samson, Ayla Jean Yackley and Funja Güler report

Vladimir Putin’s fifth term as Russian president will see increased domestic repression, continued aggression in Ukraine and efforts to consolidate Moscow’s position across much of the non-western world, Angela Stent writes for the United States Institute of Peace

Recommended newsletters for you

Are you enjoying Europe Express? Sign up here to have it delivered straight to your inbox every workday at 7am CET and on Saturdays at noon CET. Do tell us what you think, we love to hear from you: europe.express@ft.com. Keep up with the latest European stories @FT Europe

Also Read More: World News | Entertainment News | Celebrity News